Times are tough for some households and I sometimes forget that as I go about my day-to-day. I recently had a sobering reminder as I looked at a letter from our bank regarding part of our mortgage rolling off a fixed rate.

Almost $150,000 of our mortgage is moving off a two year fix of 2.29% to a floating rate of 7.99% – that’s a 5.70% jump or around $8,500 extra per year in interest. Now this isn’t a sob story from me – we are in the lucky minority of households with plenty of discretionary income – but it did stop and make me think about households who are much less fortunate.

A 26% lift in mortgage arrears

Recent data from Centrix highlights that more households are under financial distress. Rapidly escalating living costs, coupled with sharply higher mortgage rates, are squeezing many household budgets to the limit. And many people are getting behind in their debt repayments as a result.

The proportion of households behind on their mortgage repayments in March was up 26% on last year, with 19,300 accounts past due. Car loan arrears were also up 3.6% year-on-year, while 10.5% of all buy now, pay later loans were in arrears. Although loan arrears are still well below their Global Financial Crisis level, the sharp increase in households getting behind in debt repayments is a worry.

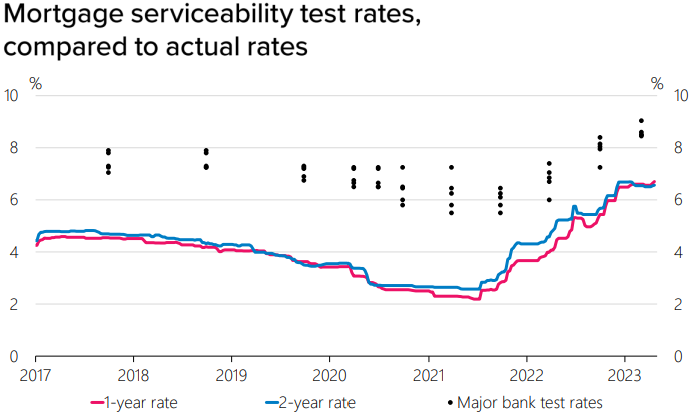

Stress test rates were too low

The Reserve Bank’s Financial Stability Report released last week also pegged my interest. The report showed households who borrowed during the period of very low interest rates between late-2020 and late-2021 were stress-tested at rates below what they are today. This is a red flag that some borrowers with high debt-to-income levels will struggle to meet their repayment obligations as they reprice onto the higher rates, and makes the Centrix data no surprise.

What irks me about bank stress testing is banks were only stress testing borrowers in the 5% to 6% range a couple of years ago. These sorts of mortgage rates were above the 2% rates that were prevailing at the time, but still well below the 9% to 11% mortgage rates we saw not that many moons ago in 2008. In my opinion, banks’ narrow focus on short-term profitability has set some households up to fail. No one should have been borrowing if a lift in mortgage rates to a level seen in recent history was going to push them into arrears.

This economist stress-tested the shit out of his family balance sheet

And this isn’t just a hindsight lecture. I am one of the households who have just been hit with a sharp lift in my mortgage rate, but that is water off a duck’s back. And the reason is that when we bought a new home two years ago, I personally ‘stress tested’ our household at scenarios many percent above where mortgages are currently and tailored our borrowing to suit.

At the time, our lending advisor probably thought I was a condescending kook. Well, I will happily wear that kook badge and only wish the Reserve Bank made more of a song and dance about realistic long-term stress testing of households. Such a move would be less about systemic financial stability and more about the financial wellbeing of individual households.