The World Economic Forum (WEF) recently warned that workers across many countries may outlive their savings by a decade or more. Analysing evidence in New Zealand shows we are in a similar boat.

Rising life expectancy is placing huge pressure on the level of savings needed to fund a good retirement. The retirement savings gap between what people have saved and what they need to save to last their retirement years has grown.

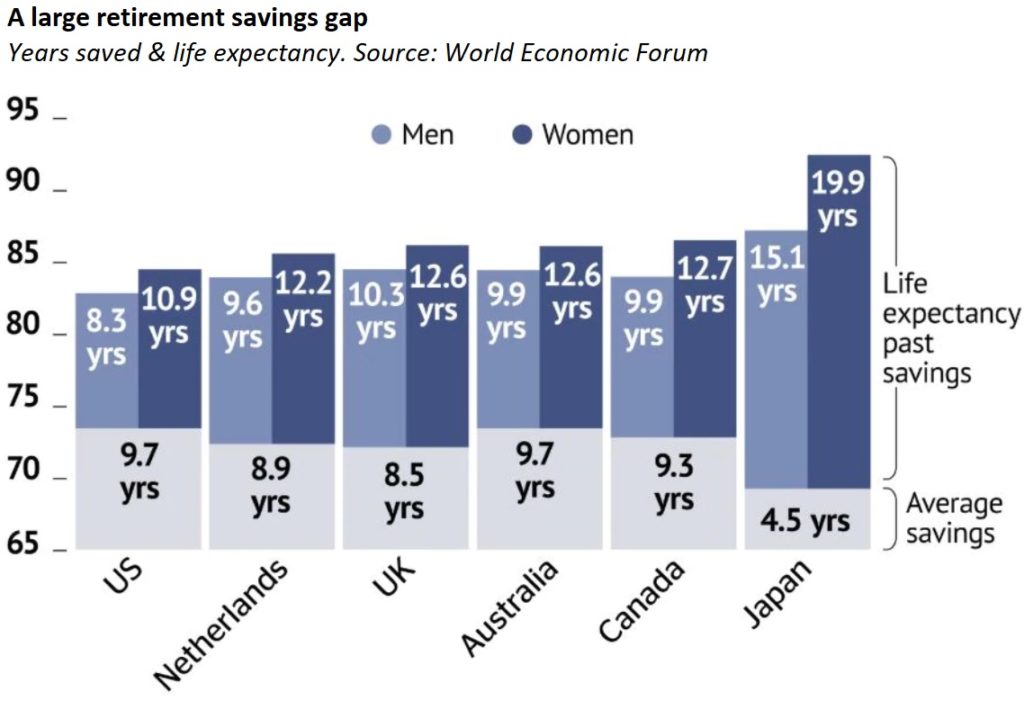

The following graph summarises analysis by the WEF into the adequacy of retirement savings among selected countries.

The retirement savings gap is about 10 years for men in the Netherlands, UK, Canada and Australia. Women in each of these nations need to get by for an extra two to three years in a financially vulnerable situation, due to their longer life expectancy.

The WEF calculates that Australians’ retirement savings will fund 9.7 years of retirement income after 65, leaving a retirement savings gap of 9.9 years for men and 12.6 years for women.

Japanese retirees face an even bigger gap. Part of the Japanese’s challenge stems from having the highest life expectancy in the world. A conservative investment style also means that savings don’t generate enough return to stretch very far, despite Japanese saving no less than other nations studied.

I decided to perform a similar analysis in the New Zealand context.

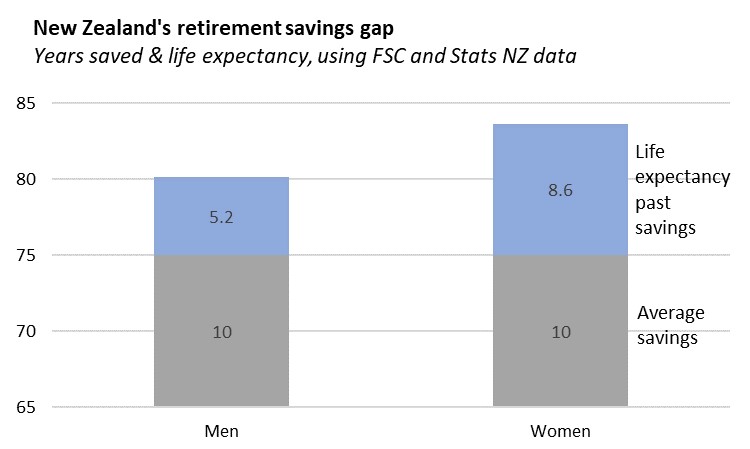

The following graph combines life expectancy data from Statistics NZ with retirement savings calculations from the Financial Services Council (FSC).

At first brush, the New Zealand experience doesn’t appear as alarming as the WEF analysis of other countries. New Zealanders have a retirement savings gap of just over 5 years for men and 8.6 years for women.

But this smaller savings gap is not driven by higher underlying savings, rather the key contributor is New Zealanders’ lower life expectancy than their peers. New Zealand men have a life expectancy of 80.2 years, while women have a life expectancy of 83.6 years. By comparison, Australian men can expect to live almost 85 years, while women will reach 87.

New Zealanders’ savings are projected to fund just the first 10 years of retirement income. The FSC analysis is based off an average retirement shortfall of $218 per week to live comfortably, which when combined with NZ Superannuation would leave retirees with just over 70% of the average weekly income. This threshold is consistent with the 70% of income used in the WEF analysis.

Real implications of inaction

The size of the retirement savings gap in New Zealand and other nations is alarming and shows a real risk of large numbers of people outliving their retirement savings. And as life expectancy increases further, people need to get their heads around retirement funds having to stretch out longer. This change in mindset will require people to think longer-term, and to start saving earlier.

The reality is that unless more is done to improve savings rates and returns, people will either need to get by on less or postpone retirement.

There are also real implications of inaction to address the savings gap for organisations that rely on the elderly to help fund their services. For example, many councils already run rates postponement schemes for elderly. Under these schemes, rates are deferred for the rest of your life and only repaid from the sale of your home or settlement of your estate.

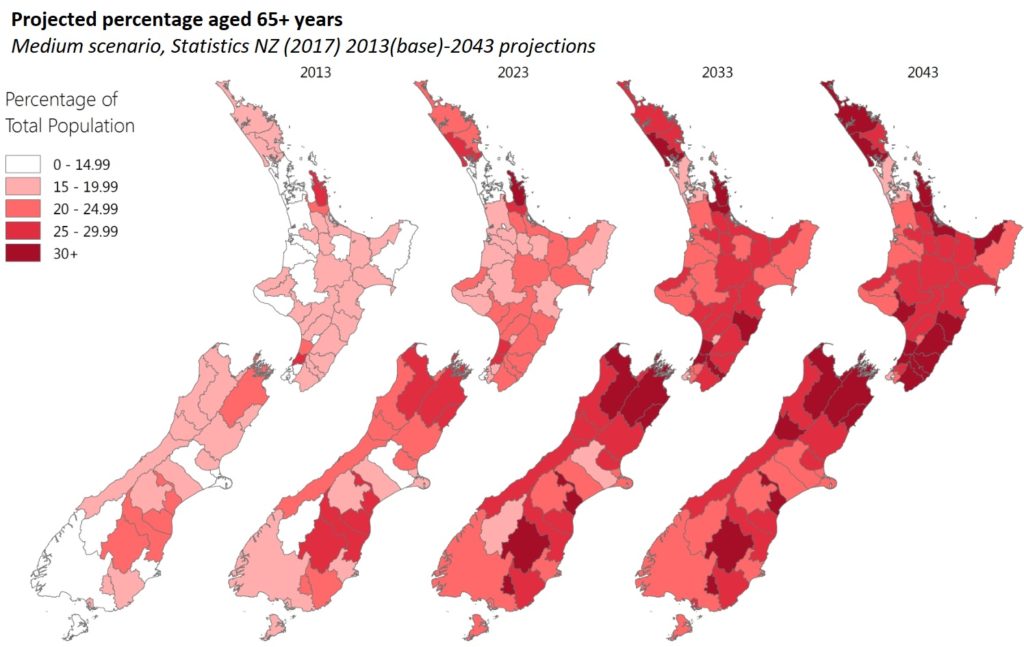

In understanding the savings gap, it is also important to think regionally. The income needed to sustainably fund retirement varies throughout the country, mainly as a result of different costs of housing. Retirees tend to congregate in different places, so concentrations of retirees are more apparent in some areas over others. These retiree concentrations can help signal a greater demand for additional support services to help mitigate risks of people entering the realm of retirement income distress.

The release of Census 2018 data on September 23 provides a good opportunity for exploring the financial and social wellbeing of elderly in your local area. Please get in touch if you want to discuss options for understanding the situation of elderly in your community.