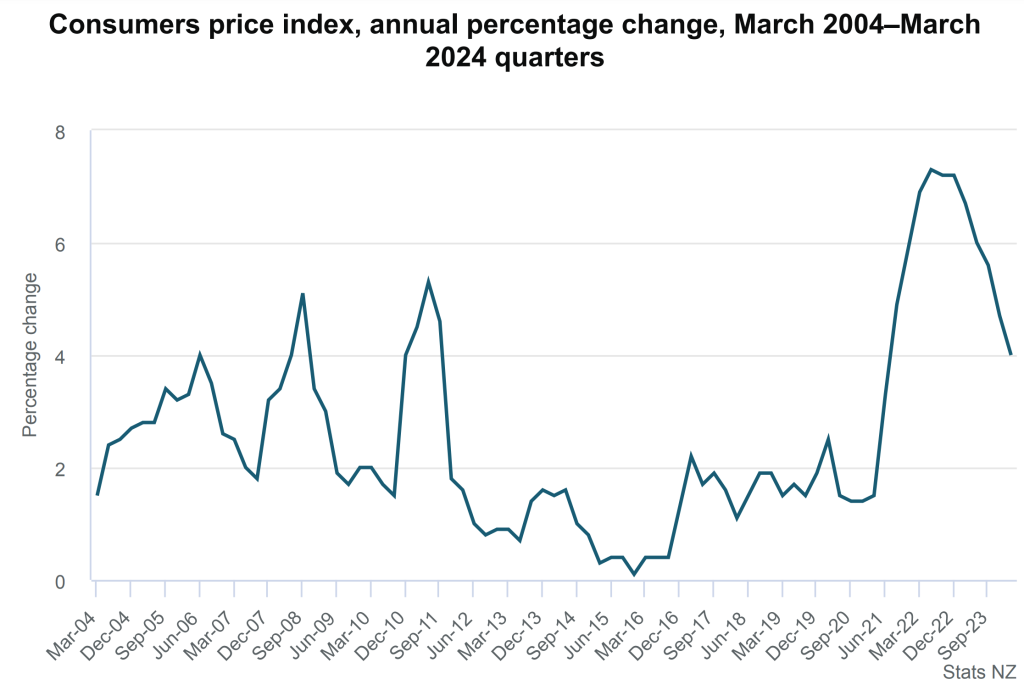

Inflation to March was 4.0%pa, down from 4.7%pa in December – its lowest rate since June 2021. At first blush, this appears to be a great result and, while lower inflation is something to celebrate, there were still pockets of concern.

The fall in inflation was entirely due to tradeables inflation, which is driven by the prices of things that can be traded internationally and so is essentially set overseas. Tradeables inflation was sitting at 1.6%pa in March, down from 3.0%pa in December.

The problem for New Zealand is that non-tradeables inflation is still running hot – sitting at 5.8%pa, only down a mere 0.1%pa from its 5.9%pa rate in December. Non-tradeables inflation is determined by price changes to goods and services which are generally only traded domestically like haircuts, lawyers and renting a house. The stickiness of non-tradeables inflation is a persistent worry for the Reserve Bank, and until we see a pathway emerge for non-tradeables inflation to head back towards the 1-3%pa target band then we are unlikely to see cuts to the official cash rate (OCR).

I remain hopeful that cuts to the OCR can emerge by later in 2024, but today’s data reinforced that we are not quite there just yet to be sure that is how the Reserve Bank will act!