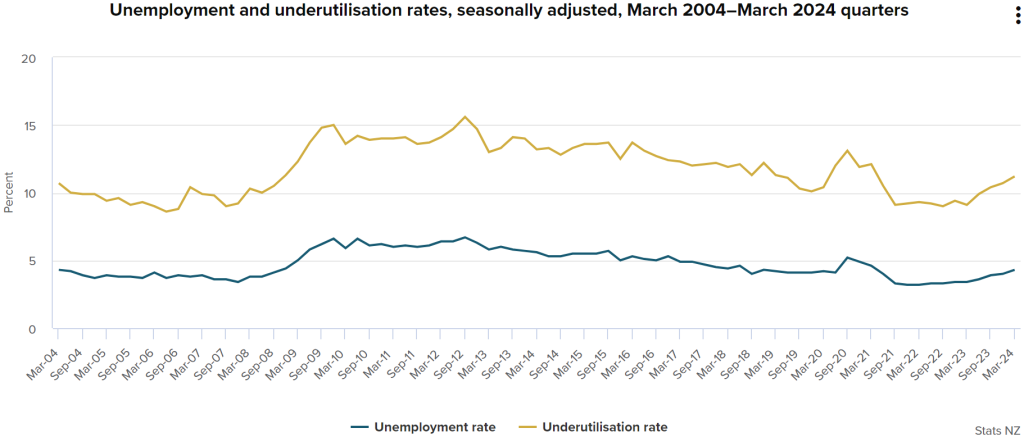

The unemployment rate in the March quarter rose to 4.3% from 4.0% in December, continuing a trend that began in June 2022. This increase, coupled with a significant rise in the underutilization rate, which encompasses both the unemployed and those seeking more work opportunities, confirms a softening in the labour market. This will hardly be news to anyone who has been searching through a rapidly depleting pool of job ads and seen the increase of “looking for work” banners on people’s LinkedIn profiles.

Employment fell by 0.2% in the March quarter, signaling that the weakening domestic economy is starting to have a tangible impact on business hiring. With indications of ongoing economic instability, further job losses are anticipated in the near future.

There’s a marked cooling in wage growth, particularly evident in the private sector where average hourly earnings have slowed to a 4.8% annual rate of growth compared to 6.6% in the previous December quarter. Although wage increases remain relatively high compared with historical levels, they’re showing a persistent downward trend over the past year and a half. It is to be hoped that this trend soon begins to mitigate non-tradeables inflation (i.e. local goods and services), which has been stubbornly high recently.

The labour market cooling in the March quarter aligns with the Reserve Bank’s expectations, making it unlikely that this result alone will prompt the Reserve Bank to lower the Official Cash Rate (OCR) in the near term. However, if the labour market weakness is coupled with any significant downward surprises in inflation or economic performance in the coming months then the Reserve Bank could begin to consider initiating OCR cuts earlier than their current projection of late 2025. The June quarter CPI statistics to be released in mid July will be particularly influential in this decision-making process.