The COVID-19 lockdown and border closures have hampered business earnings and resulted in a sharp spike in job losses. This article assesses the effects these challenges have had on the retail sector across regional New Zealand and what’s in store for the coming months. Data in the article is derived from a retail spending dataset based on transactions through the Paymark system.

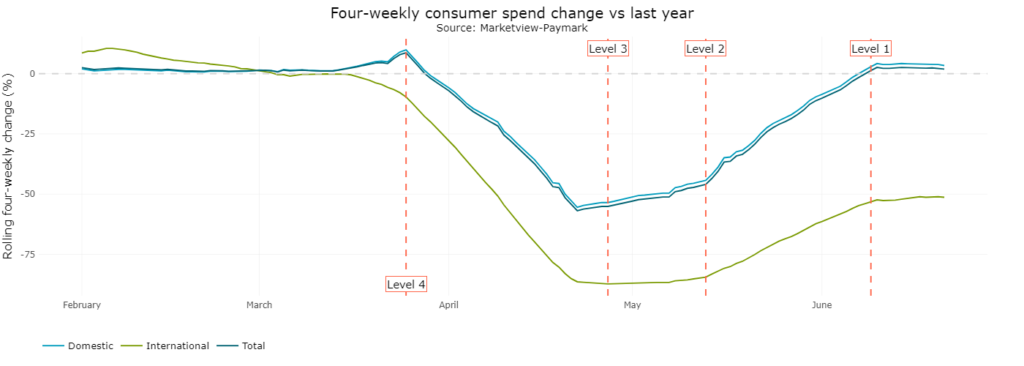

Retail spending in New Zealand reached its lowest level during the most stringent period of lockdown during April. Over the four weeks to 26 April 2020, retail spending was down 55% on its level from a year ago. Public health measures during this period saw spending fall to almost zero in all parts of the retail sector, with the exception of supermarkets and a limited amount of fuel retailing.

But spending quickly recovered to above pre-COVID lockdown levels as the country moved down the alert levels towards normality. Over the four weeks to 21 June 2020, total retail spending across the country was back up to 1.9% above its level from a year ago.

Regional retail spending growth is uneven

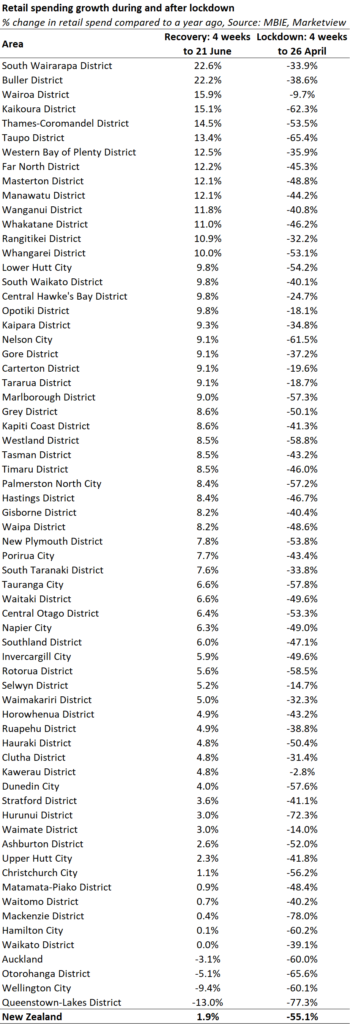

Not surprisingly, the recovery of retail spending over recent weeks has been spread unevenly across the country.

Many of the areas which have recovered the fastest are small provincial centres and places that are prime destinations for weekend getaways for kiwis. Many of the provincial centres were relatively insulated from the economic fallout of COVID-19 by their large agricultural sectors which have continued to earn healthy revenue through the pandemic. The reality is that even in such troubling times, the world has to eat, and so our fruit, dairy and meat exports are in high demand.

Weekend getaway destinations for people wanting to get out of the major urban centres, such as South Wairarapa, Kaikoura, Thames-Coromandel and Taupo have also seen a sharp recovery in spending. These areas have been able to capitalise on higher spending from domestic visitors, at a time of the year when they wouldn’t be getting many foreign tourists anyway.

At the other end of the scale, there are some places that are still lagging, with retail spending over the past month well down on a year ago. These areas are Auckland, Wellington and Queenstown-Lakes.

In the case of Wellington, much of the blame for retailers’ woes can be levelled at major public and private sector employers who have kept staff working from home. The effect has been higher spending growth around places within Wellington’s commuter belt where the workers are holed up at home, at the expense of inner city retailers. The same holds true to a limited extent in Auckland, with steeper job losses also subduing households’ willingness to spend.

Queenstown-Lakes’ economy normally derives approximately two thirds of its economic activity from visitors, with most of these coming from overseas. New Zealand’s tourism mecca is unlikely to see a return to positive retail spending growth, no matter how many kiwis visit the resort, until there is a reopening of the borders to visitors from Australia and ultimately the rest of the world.

These trends are summarised in the following table.

Will spending growth be maintained?

The recovery in retail spending in most parts of New Zealand is particularly reliant on high levels of homeware and clothing spending at present. But hospitality spending in many places has crept to close to or just above its pre-Covid level. Household spending in supermarkets remains strong, while fuel spending declines reflect lower petrol prices.

The high level of reliance from the retail sector on homeware and clothing represents a key area of risk over the coming months. Much of the demand for these types of goods is based on pent-up demand for things that could not easily be purchased during lockdown and so will eventually wane.

A sustained recovery of retailing will be contingent on a number of factors, including households’ financial positions and a continued willingness for kiwis to get out and explore their country. As the initial euphoria of Level 1 eases and a second wave of job losses occur once more people come off wage subsidies, there is a risk of some weakness ahead for retailers.