The Trans-Tasman bubble will not be a silver bullet for every tourism destination over the winter months.

Put simply – many kiwi destinations may struggle to attract Aussie travellers during the colder months, and instead will miss out on New Zealanders who head to warmer destinations across the ditch.

Of course, there will be major exceptions, like Queenstown, but by and large, it won’t be until summertime that the net gains from Australian tourists are fully realised in all parts of the country.

With this context in mind, this article looks at selected visitor spots across New Zealand over the winter months (defined here as June to September). It assesses what might happen if we assume that most of the growth in domestic tourism from last year – aka ‘the sugar rush’ – was simply pent-up demand from people with nowhere better to go than explore their own backyard.

Given this assumption, let’s imagine a scenario where 60% of the extra domestic spend from last winter heads to Australia, while in return Australian visitation to New Zealand recovers to 60% of its usual level over winter. Sure this is a fictitious example, but bear with me and let’s consider what implications it has for visitor destinations through the regions.

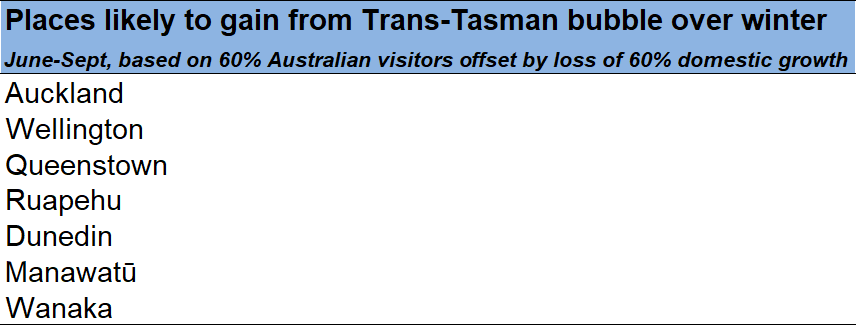

The winners

The only places under this scenario to gain materially during the winter months are our two biggest cities, followed by our most popular ski destination – Queenstown. There are also modest net gains to other winter destinations, such as Ruapehu and Wanaka, while businesses servicing visitors in Dunedin and the Manawatū may also stand their ground.

In dollar terms, the net gains for Auckland in this scenario could be close to $150 million compared to winter last year, while for Wellington they would be around $40-50 million.

Queenstown would only gain $20-25 million in net terms compared to winter last year if 60% of the usual winter volume of Australians visit and 60% of the domestic growth from last year does not return. However, the potential size of the prize for Queenstown could be huge if Australian visitation returns to 100% of normal this ski season. In such a scenario, the net gains over the winter months to Queenstown would be in the order of $125 million compared to last year.

The losers

Unfortunately under the scenario outlined in this article, most of the rest of the country is likely to lose in net terms over the winter months. The following table lists the 10 areas that would stand to lose the most.

At the top of the list are Northland and Taupō. But these two places have had good summers and are used to slower winters so will weather the storm until visitor flows ramp back up into these locations come spring and summer.

More worrying is that the next biggest losers over the winter months are West Coast, Mackenzie and Fiordland. These three places look set to each lose $10-15 million compared to last winter if only 60% of Australian visitors return over the winter months and they lose 60% of last year’s domestic growth. Although falling just outside of the 10 most affected places in dollar terms, Kaikōura (14th worst affected) will lose approximately $5 million in net terms compared to a year ago.

The perverse thing for these areas is that it has already become apparent over recent months that they are among New Zealand’s most struggling visitor destinations. The bubble looks set to intensify their short-term pain unless Australians completely change their behaviour over winter.

What could flip this on its head?

This article has painted a picture that the Trans-Tasman bubble is not going to be the saviour of the tourism industry over the winter months. There are only a few places – mainly ski destinations and urban getaways that stand to benefit. Most of New Zealand’s visitor attractions are not meccas for Australian tourism over the colder months, and instead could lose in net terms as kiwis head across the ditch. The upshot is that the government is still likely to need to open its wallet and support people in these struggling tourism communities until the busier summer months approach.

But there is still one thing that could flip this result on its head, and that is if visitor behaviour dramatically changes.

What if Australian visitation returns to business-as-usual, instead of simply recovering to 60% of its usual volume this winter? Or what if Australians travel like crazy, given that they currently don’t have anywhere else in the world to go? Australia has five times the population of New Zealand, so a small shift in their willingness to travel Aotearoa could quickly change the game for many of the visitor destinations that risk losing in net terms over winter.

Recent research by Tourism New Zealand has identified a pool of 800,000 Australians who intend to visit New Zealand over the next six months. If such a scenario did indeed unfold then Australian visitation over the June and September quarters could instead be 15% above its pre-Covid level.

But before we get too ahead of ourselves, we need to bear in mind it’s not just a matter of demand. Just as pivotal for a quick recovery will be the ability of airlines and visitor destinations to quickly scale back up their capacity to deliver their product.

How quickly this ramping up of capacity can occur remains to be seen, so over the coming months as I evaluate demand, I will also be keeping a watchful eye on the supply side. In the meantime, my advice to economic development practitioners in visitor destinations would be to keep in close contact with your tourism operators to keep abreast of their ability to supply their customers. It is likely that there will be an increased need for advocacy regarding workforce issues over the months ahead and so its best to keep ahead of these challenges as much as possible.